EPF Withdrawal Rules in 2026: Everything You Need to Know

The Employees’ Provident Fund (EPF) is one of the most trusted savings schemes for employees in India. It ensures that workers have a safe and secure financial future post-retirement. With the recent changes in 2026, the EPF withdrawal process has become more streamlined, transparent, and accessible. In this article, we will explore the key updates to the EPF withdrawal rules, their implications, and how they benefit employees in managing their finances more efficiently.

What’s New in EPF Withdrawal Rules for 2026?

The year 2026 marks a significant overhaul in how employees can withdraw their EPF funds. The government has introduced several changes aimed at making the process faster, simpler, and more user-friendly. Below is a detailed breakdown of these updates:

Let’s dive deeper into these updates.

Digital EPF Withdrawal: A Game-Changer

In 2026, EPF withdrawals have been made easier by introducing a digital withdrawal system. Employees can now access their EPF balance through UPI or ATM, making it a more accessible option during emergencies or urgent financial needs. This eliminates the need for lengthy paperwork, manual approval processes, and waiting periods that often slowed down the withdrawal process.

By providing this instant access, employees can get their funds faster for emergencies like medical expenses, education, or urgent personal needs. The digital system is expected to significantly reduce the administrative burden, ensuring a smooth experience for EPF members.

Simplified Categories of EPF Withdrawals

Previously, EPF withdrawal rules involved multiple categories with different conditions. The new rules, however, have simplified the process into three major categories:

Important Needs

Employees can now withdraw EPF funds for essential needs like medical emergencies, education, or marriage. This category has a clear structure, allowing members to access funds quickly for these critical events.

Housing Needs

If you need to buy a house, build a home, or repay a housing loan, you can now withdraw EPF funds under this category. It’s a straightforward way to use your retirement savings for a significant investment.

Special Circumstances

This category is for unforeseen emergencies such as accidents, natural disasters, or other critical life events. The simplified process ensures employees can quickly access their funds during such times.

How Much Can You Withdraw from EPF in 2026?

Under the 2026 EPF withdrawal rules, employees are allowed to withdraw up to 100% of their eligible EPF balance. This includes both the employee’s and the employer’s contributions, along with the accumulated interest on the account.

However, a key aspect of this change is that at least 25% of the balance must remain in the account. This ensures that while employees can access funds in times of need, a portion of their savings remains protected for long-term retirement security. This balance between liquidity and retirement savings is designed to protect the financial future of workers.

Minimum Service Requirement for EPF Withdrawals

To make partial withdrawals more accessible, a 12-month minimum service requirement has been introduced. Employees must complete at least 12 months of continuous service with their current employer before making most types of withdrawals. This simplifies the rules, replacing the older system that had different waiting periods for various withdrawal types.

This update makes the EPF withdrawal process more predictable and ensures that employees can plan ahead for emergencies without being bogged down by complex eligibility rules.

Full EPF Withdrawal After Job Loss: Flexibility During Transitions

Another major change is the ability to make a full EPF withdrawal rules after 12 months of job loss. This change offers flexibility to workers who may be transitioning between jobs or facing unemployment. By making the entire EPF balance accessible after a year without employment, the rules ensure that employees have sufficient funds to manage during job transitions, all while encouraging long-term savings.

This rule provides a safety net for employees who may face challenges after leaving their jobs, whether due to voluntary resignation or layoffs.

EPS (Pension Scheme) Withdrawal Rules

The Employees’ Pension Scheme (EPS), which is part of the EPF, comes with a slightly longer waiting period for withdrawals. You can now withdraw your EPS funds after 36 months of leaving your job. This extended waiting period ensures that your retirement income is protected, helping workers maintain a stable source of income post-retirement.

While this waiting period encourages long-term savings, it also balances immediate financial needs with the necessity of preserving pension funds for retirement.

Faster Auto Settlement for EPF Advances

EPF has introduced a faster auto-settlement system for advances up to ₹5 lakhs under the updated EPF Withdrawal Rules. This update speeds up the approval and transfer process for partial claims, reducing the need for paperwork and manual approvals as per new EPF Withdrawal Rules. Employees can now get access to a large portion of their EPF funds quickly, making it easier to manage financial emergencies while following the revised EPF Withdrawal Rules.

This feature is particularly useful for urgent life events, where quick access to funds can make a significant difference.

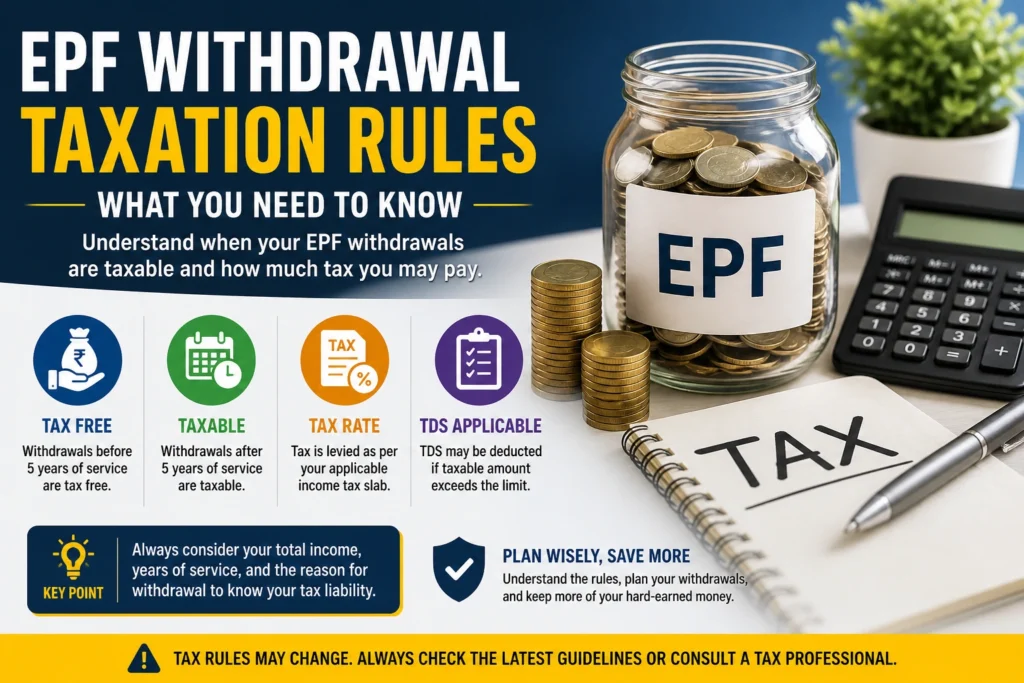

EPF Withdrawal Taxation Rules: What You Need to Know

The tax implications of EPF withdrawals depend on the duration of contributions:

Employees should be aware of these tax rules before withdrawing their funds to avoid any surprises.

Important Tips for EPF Withdrawal

Here are a few tips to ensure a smooth EPF withdrawal process:

Frequently Asked Questions (FAQs)

Final Words

With the recent updates to the EPF Withdrawal Rules in 2026, employees now have greater flexibility, speed, and transparency in accessing their savings. Whether you need funds for medical emergencies, housing, or job loss, these changes in EPF Withdrawal Rules ensure that you can get the support you need when it matters most. The new digital systems, simplified categories, and faster settlements under the updated EPF Withdrawal Rules mark a significant step forward in improving the EPF experience.

By staying informed and understanding these rules, you can make the most of your EPF account, ensuring that your financial future remains secure while also addressing immediate needs.